By Lyn Tukei

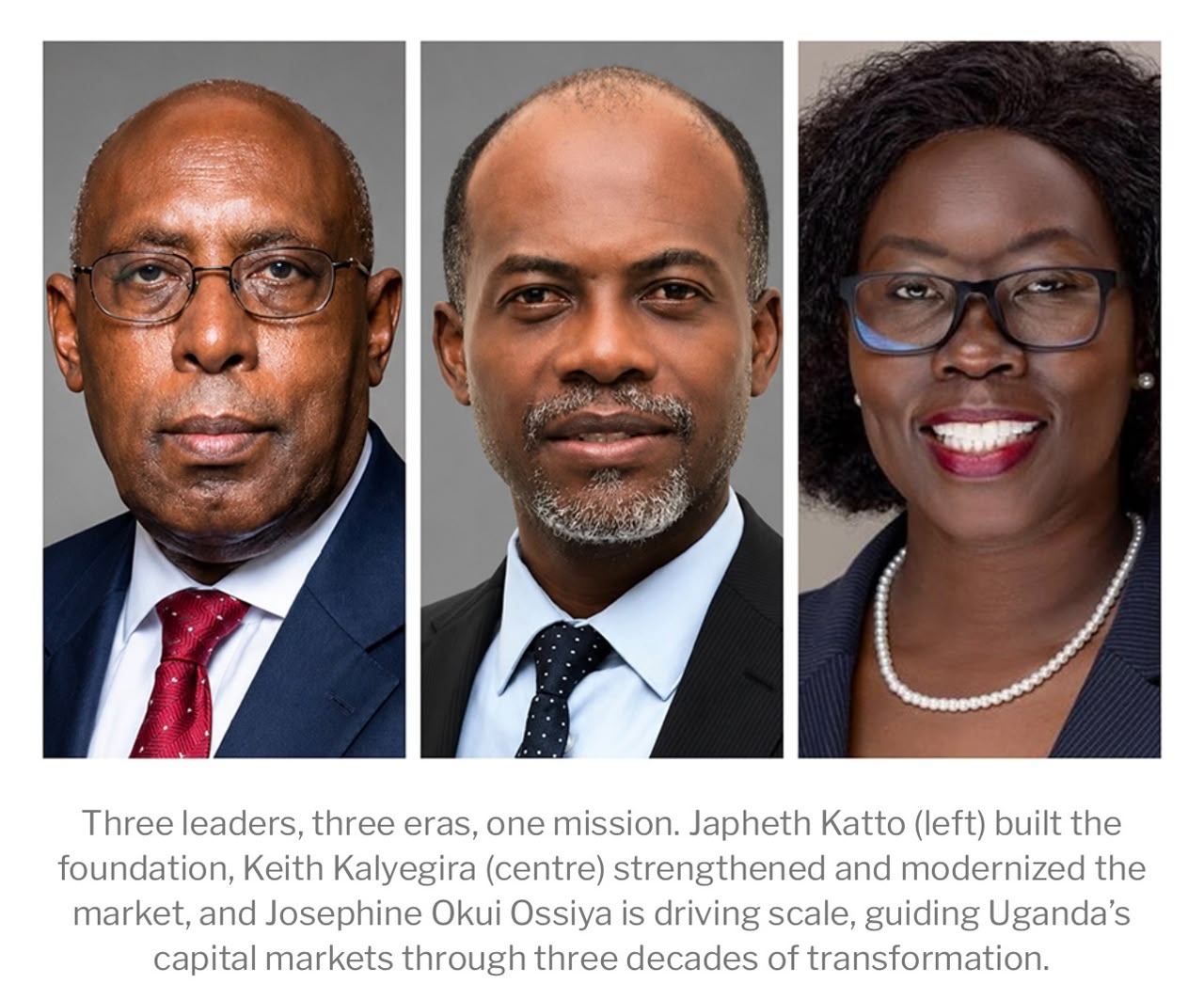

As the Capital Markets Authority (CMA) marks 30 years with a milestone celebration scheduled for Thursday, 8th October 2026; the three people who have led it, Japheth Katto, Keith Kalyegira, and Josephine Okui Ossiya, sit at different points on the same arc: Founding, Consolidation, Scaling. Together, their stories tell how Uganda built a market from scratch, and where it is headed next.

In January 1998, the Capital Markets Authority occupied the ‘zero floor’ (basement) of the Bank of Uganda’s new building. The space was modest. So was the headcount. Two technical staff seconded from the Bank of Uganda’s Domestic Financial Markets Department, Stephen Kaboyo and Simon Rutega, had been holding fort, supported in a part-time capacity by Wasswa Kajubi.

The first full-time employee at CMA, in the literal sense, was Geoffrey Karema, who had moved across from a messenger’s role at the central bank. When Japheth Katto walked in as the new Chief Executive Officer, he was, by his own telling, mistakenly issued employee identification number one. The “real number one,” he is quick to point out, was Karema.

That small administrative slip captures something true about CMA’s beginnings. The institution was being assembled in real time by a handful of people, under a board chaired by Governor Emeritus Leo Kibirango (the former Governor of the Bank of Uganda (BOU)), that had to take on far more operational responsibility than a board normally would. There was simply nobody else to do the work.

The Governor of BOU at the time was Charles Kikonyogo, who also sat on the board. He was keen for CMA to be an independent institution and therefore supported the move outside of the central bank. This idea was also wholeheartedly supported by the then Permanent Secretary to the Treasury (PSST), the late Prof. Tumusiime Mutebile.

The year before Katto joined, the foundations had already been laid. The Uganda Securities Exchange had been licensed in 1997, brokers had been licensed, and the market’s first product, the East African Development Bank bond, was on the books.

The Founding

Katto’s era was, above all, about institution-building. His task was to build something where nothing had been. Think of all the challenges and opportunities business startups face. The first IPO, Uganda Clays in March 2000, opened the equity market. This IPO was such a big deal that it warranted a public holiday. Other IPOs followed: British American Tobacco (BAT) Uganda and Bank of Baroda in October 2000 and November 2002 respectively. Stanbic, DFCU, UMEME, and New Vision (NV) were also introduced. To emphasize how significant these were, the NV IPO was launched by President Yoweri Kaguta Museveni in Mbale, where he also bought shares.

Cross-listing was first put on the agenda. So was the demutualisation of the Uganda Securities Exchange, an idea Katto would champion long before it became conventional thinking. The cross-listings introduced were EABL and Kenya Airways, followed by Equity Bank and Jubilee Insurance.

Andrew Owiny, who led MBEA Brokerage Services, handled most of the formative transactions on the sponsoring broker side. In the months and years that followed, more bonds would come under his leadership: Kakira Sugar Works, Standard Chartered Bank, DFCU Bank, and Stanbic Bank. By 2006, Stanbic Bank’s listing had given the exchange a financial-sector anchor. The Stanbic fixed-rate bond, issued just before market interest rates climbed, would go on to be one of the early profitable trades that signalled the market was open for business.

Behind the deals, Katto and the pioneer board, which included Sarah Walusimbi, Billy Kainamura, and Twaha Kaawaase, laid the institutional scaffolding: the Collective Investment Schemes regime in 2003, an Investor Compensation Fund under the Act, and a corporate governance framework.

Founding was never easy. There was the challenge of recruiting a technical team in an industry new to the country. The likes of Candy Wekesa Okoboi and Miriam Ekirapa Musaali were recruited on the legal and compliance side; Anne Mpendo and Joseph Lutwama on research and market development; and the late Anne Kyohairwe Muhangi leading public education. These were trained and later became some of the few experts in the capital markets field at the time.

One of the big priorities was to create awareness in a totally new market. Katto initiated the first Kikonyogo Capital Markets Awards, a quarterly magazine, a public education programme, and the inclusion of capital markets in the secondary school syllabus. He also championed the Capital Markets Secondary School and University Challenge, as well as a training programme for journalists.

In the area of regional integration, CMA really punched above its weight. Katto’s leadership played an active role in both regional and international presence. Regionally, the East African Securities Regulators Authority (EASRA) came into being on 5th March 1997, with peer regulators in Kenya and Tanzania. CMA also obtained membership of IOSCO and hosted the IOSCO Africa Middle East conferences. CMA then signed MOUs with a number of regulators, including those in Nigeria, Ghana, and Zambia. Mr. Katto was the Vice Chair for the Africa Middle East Regional Committee of IOSCO.

He was Chairman of the Ministry of Finance committee on pension liberalisation and regulation, work that resulted in the formation of URBRA. One of his personal beliefs, which he strongly advocated, was the consolidation of regulation of the financial services sector. His idea was to have one strong non-bank regulator, because he believed there were overlaps and consolidation would reduce duplication of roles such as public education. However, this idea has not yet yielded fruit.

By the time Katto handed over, CMA had moved from being a two-desk operation in a basement to being a recognised regulator with a staff of 24 professionals of proven competence; a published syllabus; a public education programme reaching from secondary schools to universities; a stock exchange that had hosted several IPOs and bonds; an established board, chaired in succession by distinguished figures (Governor Emeritus Leo Kibirango, Prof. Hajji Twaha Kaawaase, and CPA Grace Jethro Kavuma), that no longer needed to do management’s job; and a community of intermediaries who knew the rules of the game.

The Consolidation

If Katto’s era was about laying foundations, Keith Kalyegira’s was about confronting the limits of what those foundations could carry.

He took office with a public set of targets. On 16 January 2014, at Katto’s farewell, Kalyegira introduced himself to the market by committing to four things: adding UGX 6 trillion to the market capitalisation of the Uganda Securities Exchange; raising an additional UGX 600 billion in bonds; putting in place a client service charter; and increasing public understanding of the capital markets.

By the time he stepped down nearly a decade later, the scoreboard read like this: UGX 8.1 trillion had been added to the market capitalisation of the USE, driven by the listings of MTN, Airtel, and Cipla, which between them brought in 27,600 new investors. UGX 110 billion was issued in private and public debt, well short of the bond target. The client service charter was launched in 2015 and has been adhered to for every equity offer since. And 65,000 new investors put more than UGX 2.2 trillion into the debt and equity markets through Collective Investment Schemes, more than making up, by his own assessment, for the shortfall in corporate debt.

Kalyegira took office at a point when Uganda’s capital markets had visibility but not yet depth. Listings had happened, but liquidity in the secondary market was thin. Licensed dealers existed, but few were actively making markets. The investor base was institutional and concentrated. And the macroeconomic environment (high government borrowing, elevated real interest rates, modest household savings) was, by his own diagnosis, structurally unfriendly to capital markets growth. Research, he would later point out, shows that capital markets tend to thrive in economies where real interest rates sit below two to three percent. Uganda’s were rarely there.

His response was to push, simultaneously, on policy, structure, and product.

Between 2017 and 2023, he and his team made a sustained case for public ownership in the telecommunications sector, working with policymakers around the renewal of telecom licences. The proposition was carefully framed: not compulsory listing, but encouraging local and public ownership as a form of corporate citizenship. That conversation eventually contributed to the MTN Uganda IPO in 2021, which remains the largest in the country’s history. Similar conversations were attempted with the banking sector, although those did not progress for regulatory and policy reasons.

Kalyegira also championed pension reform, arguing, in three connected pillars, for the establishment of a dedicated pensions payments regulator; a structural shift from lump-sum payouts to a one-third lump-sum and two-thirds monthly pension model; and the liberalisation of the sector to allow new retirement benefit schemes beyond NSSF. The logic was straightforward: capital markets need a deep pool of patient domestic capital, and pensions are the most natural source. Cipla’s IPO, with approximately 98 percent institutional subscription, illustrated the point; institutional investors were carrying the market, and the institutional base needed to grow.

He was equally candid about what was not working. Global stock exchanges, he observed, were experiencing declining listings as private equity offered an easier path for companies seeking growth capital. Uganda’s bond market lacked the transparent, centralised trading infrastructure of the kind Thailand had built. Stamp duty and other regulatory frictions were making private infrastructure investment harder than it needed to be. Oil and gas, while a clear opportunity, would more realistically yield listings among local service providers and supply-chain companies than among the multinationals operating the major fields.

But perhaps his most enduring contribution was a quiet reframing of what success looks like. “For a long time, the symbols of success of the regulator have been how many companies are listed,” he reflected on his departure. “While listings have been achieved, the purpose for the issuance of securities and listings is much more important.” The capital markets, in his view, are first and foremost the place where debt and equity are issued to finance the growth of companies, through public offers with or without a listing, through private placements, through engagement with private equity. Listings are a means, not the measure.

He left the market with a set of reflections, one for each year of his service. Among them: that retail savers rarely provide more than USD 15 million in any single public offer, which means typical deal sizes should sit in the UGX 5 to 20 billion range, with asset managers willing to underwrite them; that with government paying a 14 percent coupon for ten years, any business seeking capital markets funding should be able to consistently generate returns above 20 percent per annum to attract investors; that financial intermediaries should not apply for licences unless they can break even within 24 months and finance the business until they do; that a 10 percent annual staff turnover (three out of thirty) is too high, and that a dedicated capital markets training institute, funded by a small industry levy, would help sustain the talent pipeline; and that the CIS industry today is the size of the banking sector in the year 2000, and that the regulator’s capacity must grow with it.

The thread running through his tenure was a defence of regulatory independence. The job of a market regulator, he argued, is not to promote listings to the point of appearing biased; it is to maintain strict investor protection and high disclosure standards, and to let credibility do the work of attracting capital.

The Scaling

Thirty years ago, the Capital Markets Authority was a fledgling institution operating from modest offices, staffed by a handful of pioneers tasked with building something Uganda had never truly had before: an organized capital market.

Today, the institution regulates over 160 licensed market participants, oversees trillions of shillings in assets, protects hundreds of thousands of investors, and sits at the centre of Uganda’s long-term economic ambitions.

The transformation has been remarkable, yet the most important chapter may still lie ahead.

For Josephine Okui Ossiya, Chief Executive Officer of the Capital Markets Authority, the challenge is no longer building the market. It is scaling it; and scaling, as every leader knows, is often harder than starting.

By the time she assumed leadership of the Authority, the market had reached an inflection point. The foundations had been laid, regulatory credibility had been established, investor confidence was growing, new products were emerging, and participation was increasing.

But the question confronting the institution was no longer whether capital markets could work in Uganda. The question had become whether they could grow quickly enough to support Uganda’s aspirations of becoming a USD 500 billion economy by 2040.

That challenge now defines the Authority’s third decade.

“At thirty,” Ossiya says, “we are no longer simply building a market, we are building the future architecture of Uganda’s capital formation ecosystem.”

It is a statement that captures both the opportunity and responsibility of leading Uganda’s capital markets at a moment when the country is pursuing one of the most ambitious economic transformation agendas in its history.

The numbers tell a compelling story. By December 2025, Collective Investment Schemes had accumulated assets under management exceeding UGX 5.6 trillion, segregated fund assets had grown to nearly UGX 6 trillion, and domestic market capitalization on the Uganda Securities Exchange had surpassed UGX 15 trillion.

More than 220,000 Ugandans now held funded Collective Investment Scheme accounts, over 235,000 investors-maintained Securities Central Depository accounts, and what was once a niche financial ecosystem has steadily evolved into an increasingly important pillar of Uganda’s financial architecture.

Yet for Ossiya, these figures are not the destination. They are evidence of potential, potential that remains largely untapped, potential that must now be converted into economic impact.

For a country seeking rapid industrialization, infrastructure expansion, enterprise growth, job creation, and increased productivity, access to long-term patient capital is no longer optional. It is essential, and that is where capital markets enter the national conversation.

The Authority’s Strategic Plan for 2025/26 to 2029/30 carries a deliberately ambitious theme: Catalyzing Participation and Harnessing the Capital Markets.

Its purpose extends beyond institutional performance. It is directly linked to Uganda’s Tenfold Growth Strategy and the national objective of expanding the economy to USD 500 billion by 2040. Historically, economic growth has relied heavily on banking sector financing, yet no economy has successfully financed transformational growth through bank lending alone.

Large-scale development requires patient capital. It requires equity, it requires long-term debt, and it requires sophisticated investment vehicles capable of matching long-term savings with long-term investment opportunities.

“The capital that capital markets can mobilize will be a critical component of funding Uganda’s development strategy,” Ossiya explains. “Capital markets are indispensable in mobilizing long-term capital.”

The future role of the Capital Markets Authority is not merely regulatory. The institution is increasingly becoming a strategic enabler of national transformation.

The strategy underpinning this transformation rests on five interconnected priorities.

The first is participation. Despite significant progress, Uganda remains underpenetrated relative to regional peers. CMA’s ambition is therefore bold: increasing funded Collective Investment Scheme accounts to one million within five years. Such growth would fundamentally alter the profile of domestic savings and investment in Uganda.

The second priority is diversification. Currently, government securities dominate investment allocations. While these instruments provide stability and safety, a mature market requires broader investment opportunities. The Authority is therefore focused on accelerating the development of alternative products, including Real Estate Investment Trusts (REITs), infrastructure bonds, green bonds, asset-backed securities, private capital solutions, and Islamic finance instruments.

The third priority is expanding the supply of investable opportunities. Markets cannot deepen without assets, and a market cannot achieve sustained liquidity when the number of listed companies remains limited relative to the size of the economy.

To address this challenge, CMA is actively supporting issuer readiness programmes while strengthening initiatives such as the Deal Flow Facility, which seeks to connect promising enterprises with investors and capital providers.

The fourth priority is regional integration. Capital increasingly moves across borders. As Chairperson of the East African Securities Regulators Association (EASRA), Ossiya sees regional harmonization as an economic necessity. Integrated markets create larger pools of capital, greater liquidity, and enhanced investor confidence.

The fifth priority is sustainability. The future of finance is increasingly shaped by environmental, social, and governance considerations. Uganda’s capital markets are positioning themselves accordingly through ESG disclosure frameworks, sustainable finance guidelines, green finance instruments, and the introduction of Islamic finance products.

Collectively, these priorities represent a blueprint for market transformation.

Perhaps the most distinctive aspect of Ossiya’s leadership style is her willingness to place measurable commitments in the public domain. She identifies three milestones against which investors and stakeholders should judge the Authority over the next five years.

The first is the operationalization of Uganda’s inaugural sovereign Sukuk. Such an issuance would not merely introduce a new financing instrument. It would position Uganda within the global Islamic finance ecosystem and open access to significant pools of Sharia-compliant capital.

The second milestone is the expansion of Collective Investment Scheme assets beyond UGX 12 trillion. Given recent growth trajectories, the target is ambitious but attainable.

The third is the successful issuance, listing, and trading of a transformational market instrument, whether a REIT, infrastructure bond, green bond, or another innovative product.

“They are commitments,” Ossiya says. “Our Strategic Plan and our work programmes are aligned to achieve them.”

Many organizations produce excellent strategic plans. For Ossiya, execution is where strategy becomes meaningful. “A plan without implementation infrastructure is simply a wish list.”

The Authority’s approach reflects this philosophy. Strategic objectives are translated into annual work plans. Performance is monitored quarterly. Resources are aligned to priorities. Progress is reported to the Board. Accountability mechanisms are embedded throughout the institution. This focus on execution has already produced results. CMA achieved a 96 percent work-plan performance score during FY 2024/25. Its budget framework increasingly aligns financial resources with market development priorities, investor education, technology modernization, and regulatory effectiveness.

For all the progress, one challenge continues to dominate discussions around Uganda’s capital markets. Liquidity.

Ossiya speaks about it with unusual candor. “Thin equity market liquidity is one of the issues that keeps me awake at night.”

The concern is well-founded. Liquidity is the lifeblood of capital markets. Without it, investors struggle to enter and exit positions efficiently. Without it, price discovery weakens. Without it, institutional participation remains constrained. And without it, market growth eventually reaches its limits.

“A market where price discovery is difficult and exit is uncertain does not attract the institutional investors we need to scale.” The challenge becomes even more apparent when viewed against Uganda’s economic potential. A USD 63 billion economy supported by only a handful of domestic listed companies presents a clear mismatch between economic activity and capital market depth.

Addressing the problem requires simultaneous action on three fronts: increasing the supply of securities through additional listings, expanding investor demand through participation and education, and strengthening market infrastructure through mechanisms such as market-making and liquidity enhancement programmes.

If participation and liquidity are the visible goals, regulation remains the invisible foundation upon which market confidence depends. In 2025, CMA implemented a significant regulatory modernization exercise. The objective was to create a regulatory framework that protects investors while enabling innovation and growth. Alongside these reforms, the Authority launched a Regulatory Sandbox to support fintech innovation and emerging technologies. Work is also progressing on a crowdfunding framework designed to expand financing opportunities for small and medium-sized enterprises. Simultaneously, CMA participates in a multi-agency effort to develop an appropriate framework for digital assets and emerging financial technologies.

Innovation is not something regulators can afford to observe from the sidelines. It must be understood, supervised, and harnessed.

At its core, every capital market is built on a single foundation: trust. Without trust, investors do not participate. Without participation, capital does not form. And without capital formation, markets cannot fulfil their developmental role. Investor protection therefore remains central to CMA’s mandate.

The Authority continues to strengthen the Investor Compensation Fund while enhancing surveillance, disclosure enforcement, and market monitoring capabilities. Cross-border collaboration through EASRA has become increasingly important as regional markets become more interconnected. “Insider trading in a cross-listed security does not respect national borders,” Ossiya notes. “Our regulatory response cannot either.” Modern capital markets require modern regulatory cooperation.

Regional comparisons provide both encouragement and perspective. Kenya continues to maintain larger market capitalization levels, deeper participation rates, and more developed investment ecosystems.

Yet Uganda’s recent growth trajectory has been among the strongest in East Africa. Market capitalization growth exceeded twenty-five percent in 2025, Collective Investment Schemes continued expanding rapidly, and investor participation accelerated.

Macroeconomic stability improved. International confidence strengthened following Uganda’s sovereign outlook upgrade. Rather than attempting to replicate larger markets, Uganda is pursuing a differentiated path: a high-growth frontier market, a hub for sustainable finance, a gateway for Islamic finance, a digitally accessible market, and a regionally integrated investment destination.

One Arc

Viewed across thirty years, the history of the Capital Markets Authority can be understood as a single story unfolding across three distinct chapters.

The first chapter was institution building, the second was reform and modernization, and the third is scale.

Together, the leaders who have guided the Authority represent successive stages of the same journey. The pioneers established credibility, their successors strengthened resilience, and the current leadership is focused on expansion. Different leaders, different contexts, one institution, one mission, and one evolving story.

In March 2000, the Uganda Clays IPO demonstrated what capital markets could become. Two decades later, the MTN Uganda IPO demonstrated how far the market had travelled. And the next chapter will be measured on an entirely different scale.

Not in billions, but in trillions.

Not by the number of regulations issued, but by the amount of capital mobilized.

Not by the size of the institution, but by its contribution to Uganda’s development.

Thirty years after its establishment, the Capital Markets Authority stands at a pivotal moment. The foundations have been laid, the architecture is taking shape, the ambitions are larger than ever, and the task before the institution is clear: to transform savings into investment, to transform investment into growth, and to transform capital markets into one of the principal engines of Uganda’s economic future.

Thirty years on, the foundations have held. The next thirty years will determine just how high they can build.

The writer is the Communications and Public Relations Manager at the Capital Markets Authority of Uganda